When we carry out an audit, one of the most common questions we’re asked is:

“How did you decide what to test?”

The short answer is: professional judgement, guided by materiality and risk.

Below, we explain how this works in practice and how Spondoo Audit determines appropriate audit samples.

Materiality is a key concept in auditing. It represents the maximum level of error or misstatement in the financial statements that could reasonably influence the decisions of users, such as shareholders, lenders, or other stakeholders.

In simple terms, materiality helps us answer the question:

“At what point would an error actually matter?”

Materiality is determined for the financial statements as a whole, not for individual transactions in isolation.

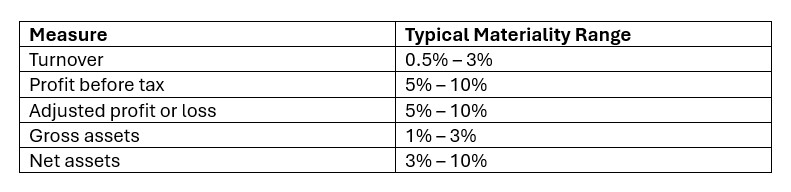

To calculate materiality, we first select an appropriate benchmark. The benchmark chosen depends on the nature of the business and what users of the accounts are most likely to focus on.

Turnover

Profit before tax

Adjusted profit or loss

Gross assets

Net assets

A profit-oriented trading company may be best assessed using profit before tax

A not-for-profit organisation may be better assessed using total income or expenditure

An asset-rich company may require gross or net assets to be the primary benchmark

There is no single “correct” benchmark — selecting the most appropriate one requires professional judgement and a clear understanding of the business.

Once a benchmark is selected, we apply a percentage to calculate overall financial statement materiality. The percentage applied varies depending on the benchmark and circumstances.

Typical Ranges Used in Practice

Around 5% of profit before tax may be appropriate for a profit-making private company

Around 1% of turnover may be more appropriate where profit levels fluctuate or are not the main focus

However, these percentages are guidelines, not rules. Higher or lower percentages may be appropriate depending on the specific circumstances.

The final materiality level may be influenced by:

Whether the business is owner-managed or has external investors

Whether the company is publicly traded

The expectations and needs of users of the financial statements

The stability or volatility of results

Regulatory or reporting sensitivities

For example, a lower materiality threshold may be applied where accounts are relied upon by external funders or regulators.

Materiality is set at the planning stage of the audit. Even where draft accounts or management information are not yet available, we establish an initial materiality based on expected figures, not simply last year’s numbers.

We may use information such as:

Prior year results

VAT returns

Management forecasts

Knowledge of changes in the business

Materiality is then reviewed and adjusted if necessary as the audit progresses.

Materiality does not depend on audit risk. Instead:

Materiality reflects what matters to users

Risk determines how much work we do

Once materiality is set, it helps us decide:

Which balances and transactions to focus on

How large our audit samples need to be

The nature and extent of audit testing

Higher-risk areas will attract more detailed testing, even if the amounts involved are below overall materiality.

Some audit approaches attempt to calculate materiality by averaging figures based on turnover, profit, and assets. We do not consider this an appropriate method.

Averaging can dilute focus and fail to reflect where the real risks lie. Instead, we:

Select the most relevant benchmark

Consider others only where justified

Clearly document our reasoning

This ensures materiality is tailored to the business, not mechanically calculated.

At Spondoo Audit, we fully document:

The benchmark selected

The percentage applied

The reasoning behind our judgement

Any changes made during the audit

This ensures our approach is robust, defensible, and compliant with auditing standards.

Our audit sampling is:

Based on clearly defined materiality

Tailored to your business

Driven by professional judgement, not rigid formulas

Adjusted as needed during the audit

If you’d like to understand more about how our audit approach applies specifically to your company, we’re always happy to explain — clearly and without jargon.

Reach out to us today.